Analysis

We’re likely stuck in an economic traffic jam for the foreseeable future.

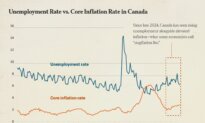

Several economists have predicted that the Canadian economy will continue to experience “Stagflation Lite” throughout most of the new year. While that doesn’t suggest an economic cliff is on the horizon, it looks like a prolonged stretch of discomfort for Canadians in 2026.

The term “stagflation” refers to the economic one-two punch of stagnation and inflation last seen in the 1970s. But because it’s “lite” it may not become as dire as the original version. For now, at least.

Think erosion, not collapse. After several years of inflation, higher interest rates, and global trade disruptions, household finances are showing signs of strain. The question facing many Canadians is how to adjust if this environment lingers.

What ‘Stagflation Lite’ Means

Traditional stagflation refers to a rare combination of weak economic growth, rising inflation, and high unemployment, often accompanied by widespread layoffs.

To fight inflation, central banks would typically raise interest rates. However, higher rates make it more expensive for businesses to borrow and grow, which can increase unemployment and further slow the economy.

The traditional way to fight unemployment is the opposite approach: lowering rates or increasing spending to stimulate growth. But injecting more money into the system can cause prices to rise even faster, worsening inflation.

According to groups like the International Monetary Fund and the Organisation for Economic Co-operation and Development, the current outlook for Canada is less severe than actual stagflation, but it still poses challenges. Frances Donald, chief economist at RBC, considers “stagflation lite” to mean that “growth is likely to be too low and inflation too high for comfort.”

Though Canada may avoid a recession, the trend isn’t likely to deliver meaningful relief to Canadians.

Persisting Pressures

All of this didn’t happen overnight, and will likewise take time to resolve. Years of higher food prices, rising housing costs, and interest rate increases have built the foundation, raising borrowing costs across the economy.

As headline inflation slows, prices aren’t likely to drop. Grocery bills, insurance premiums, utilities, and municipal fees tend to remain elevated, regardless of other factors. Even if the CIBC’s chief economist, Avery Shenfeld, is correct that prices have “crested,” it can still weigh heavily on households that have already absorbed multiple increases.

Wage growth has improved in some sectors, but it’s not consistently kept pace with living costs. That gap can leave families with less capacity to rebuild savings or absorb unexpected expenses.

Declining Investment

The economic traffic jam is worsened by a sharp retreat in business investment.

Real investment in industrial machinery and equipment recently hit its lowest level since 1981, signalling a hollowing out of Canada’s manufacturing base. This industrial implosion is driven by years of excessive regulation, a chronic lack of ambition in resource transformation, and global protectionism.

Similarly, the oil and gas sector faces significant headwinds due to red tape and regulatory uncertainty, according to a report from the Fraser Institute, which stifle growth and discourage capital inflows. This investment drought limits the creation of high-quality jobs, leaving fewer opportunities for workers even as the cost of living climbs.

Without a competitive tax regime and a sweeping reduction in red tape, Canada risks becoming increasingly irrelevant in global supply chains.

Global Trade Pressures

Global trade disputes may seem like high-level politics, but in 2026 their effects are felt at the checkout line and in the local job market. While the “trade war” between Canada and the United States peaked in early 2025, its remnants, the swelling deficit, and Canada’s investment-adverse policies have all settled into a persistent weight on the economy.

So long as tariff measures persist as bargaining chips in the 2026 negotiations, the economic traffic jam will likely continue. For the average Canadian, this means that while the threat of a total trade collapse has faded, the efficiency of the North American supply chain is gone.

And Canadians are the ones paying for the friction.

Inflation Fatigue

One of the most significant effects in recent years has been the slow drain on household resilience. Many Canadians entered the inflationary period with a savings buffer built during the pandemic. Lately, those buffers have thinned.

As savings decline, households rely more heavily on credit to manage routine expenses. Credit cards, lines of credit, and short-term financing have become coping tools rather than emergency options.

With interest rates still elevated, this borrowing is more expensive than it was only a few years ago. The result can be a sense of financial fatigue: managing your household carefully but feeling little progress.

Housing Costs

Housing remains a central factor in Canada’s economic story. While home prices have stabilized in many regions, ownership costs remain high due to mortgage rates, property taxes, insurance, and maintenance expenses.

Renters face their own pressures, with limited supply keeping rents elevated in many urban centres. Housing may no longer be driving inflation upward, but it continues to absorb a large share of household income.

And regional differences matter greatly. Canadians in smaller markets may face fewer housing pressures, but higher transportation and energy costs often offset those gains.

Where Budgets are Exposed

For average Canadians, in addition to housing costs, food, energy, and transportation remain the primary pressures on the household budget. The cost of grocery store items rose 4.7 percent year over year in November 2025, after increasing 3.4 percent in October, which is the largest increase since December 2023.

Fuel and utility costs will always fluctuate, making budgeting more difficult. Transportation decisions (such as owning a vehicle versus relying on public transit) involve trade-offs that vary widely by region. Small increases in these categories tend to have outsized effects because they are unavoidable expenses.

How Canadians Can Cope

Dramatic lifestyle changes aren’t always necessary. Basic, common-sense habits can be just as effective, like choosing store brands, planning meals more carefully, and jettisoning unused subscriptions.

Is that large purchase really necessary right now? Try prioritizing repairs over replacements. Cutting back on unnecessary spending can give you greater financial flexibility for an uncertain future. Rebuilding emergency funds, even in small amounts, and paying down high-interest debt are also good places to start.

Managing cash flow, reducing exposure to high-interest debt, and maintaining adaptable budgets are more effective than trying to adjust to economic shifts as they occur. For many Canadians, the response in 2026 may look less like sacrifice and more like a renewed emphasis on practical financial choices that quietly add up over time.

Friends Read Free

Copy

Facebook

Tweet

Friends Read Free

Copy

Facebook

Tweet