A brokerage account and an individual retirement account (IRA) are similar in some ways; both let you invest in stocks, funds, and other assets. However, they treat taxes very differently. And that difference can be worth tens of thousands of dollars over time.

If you are just starting out, the right account to open first depends on three things: whether your employer offers a 401(k) match; how much you earn; and when you will need the money. What we’re aiming to do in this article is explain both accounts clearly and give you a straightforward framework for deciding which one fits your situation.

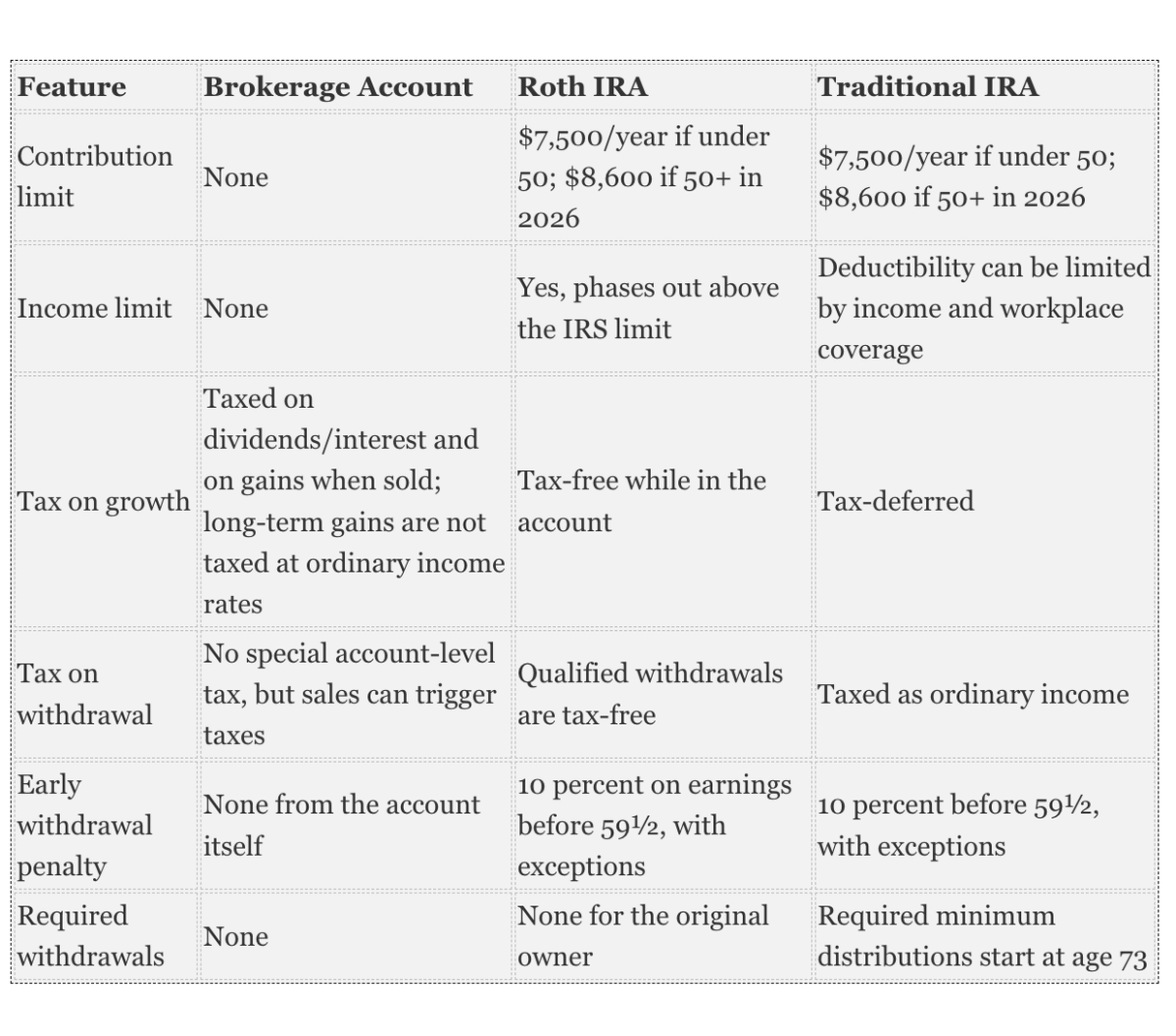

They Hold the Same Investments, but the Tax Rules Are Completely Different

This is often the deciding point, and the one most beginners skip over. A brokerage account and an IRA can hold the exact same investments (e.g., stocks, index funds, exchange-traded funds). The difference is how and when the government taxes your gains.

Think of it this way: the IRA is a special container the government created to encourage retirement saving. Put your investments inside that container, and you get tax advantages you cannot get in a regular account.

The brokerage account has no container. It is fully exposed to taxes every step of the way.

Here is what that looks like in practice:

The Brokerage Account: Full Flexibility, No Tax Shelter

A taxable brokerage account has no rules about who can open one, how much you can put in, or when you can take money out. Investing $500 or $500,000 has the same rules, and you could withdraw tomorrow without penalty.

The trade-off is taxes.

Every year, the dividends your investments pay out are taxed as income. When you sell an investment for a gain, you owe capital gains tax at your ordinary income rate if you held it less than a year, or at the lower long-term rate (0 percent, 15 percent, or 20 percent, depending on your income) if you held it longer.

That annual tax friction is called tax drag. In any single year, it’s not dramatic. But compounded over decades, it meaningfully reduces how much your money grows compared to an account where gains compound untouched.

The brokerage account’s strengths are real, though. It is the right tool when:

- You are saving for a goal less than five years away.

- You have already maxed your IRA and want to invest more.

- You want access to your money without any restrictions or penalties.

The IRA: A Tax Shelter Built for Retirement

The government offers two options for an IRA, each with different tax structures.

Roth IRA Taxes

With a Roth IRA, you contribute money you have already paid taxes on, such that:

- Your investments grow completely tax-free, and qualified withdrawals in retirement are tax-free.

- You can also withdraw your contributions (not your earnings) at any time without penalty, making it somewhat more flexible than people assume.

- There is an income limit: if you earn above roughly $153,000 as a single filer in 2025 ($242,000 if joint), your eligibility begins to phase out.

Traditional IRA Taxes

For a standard IRA, contributions may be tax-deductible depending on your income and whether you have a workplace retirement plan. Benefits include:

- Your investments grow tax-deferred.

- You pay ordinary income tax when you withdraw in retirement.

- Required minimum distributions begin at age 73.

For most people who are early in their careers and currently in a lower tax bracket, the Roth IRA is the stronger choice. You lock in today’s lower tax rate, and everything that grows from that point forward is yours tax-free.

Before Either Account: The 401(k) Match Question

If your employer offers a 401(k) and matches your contributions, that match should almost certainly come first, before any IRA or brokerage account.

A 50 percent match on your contribution is an immediate 50 percent return on your money. No investment account, no matter how tax-efficient, can compete with that. Capture the full match first, then turn your attention to the decision of choosing either an IRA or a brokerage account.

The Same Investment, Two Very Different Outcomes

Here is a concrete illustration of why the account type matters.

Suppose you invest $7,000 and it grows to $70,000 over 30 years (a realistic outcome with consistent index fund returns):

- In a taxable brokerage account, you owe capital gains tax on roughly $63,000 of gains when you sell. At the 15 percent long-term rate, that is about $9,450 owed to the IRS.

- In a Roth IRA, you owe nothing. The entire $70,000 is yours.

That is one year’s contribution. Multiply that across 30 years of annual contributions, and the difference runs well into six figures.

FAQs About Brokerage Accounts and IRAs

Can I Have Both a Brokerage Account and an IRA at the Same Time?

Yes, and many investors do. There is no rule preventing you from holding both simultaneously. A common strategy is to max your IRA contribution each year first, taking full advantage of the tax shelter, and then direct any additional investing dollars into a taxable brokerage account. You can even hold both accounts at the same brokerage platform, making it straightforward to manage them together without juggling multiple institutions or logins.

Does Opening a Brokerage Account or IRA Affect My Credit Score?

No. Opening an investment account of any kind does not involve a credit inquiry and has no effect on your credit score. These accounts are entirely separate from the credit system. Your credit score is based on borrowing and repayment behavior via credit cards, loans, and similar products. Investing, saving, and opening brokerage or retirement accounts do not appear on your credit report and cannot help or hurt your score in any way.

What Is the Deadline to Contribute to an IRA for a Given Tax Year?

You have until the federal tax filing deadline (typically April 15 of the following year) to make IRA contributions that count toward the prior tax year. For example, you can contribute to your 2025 IRA anytime between Jan. 1, 2025, and April 15, 2026. This extended window gives you time to fund your IRA even after the calendar year ends, and it also allows you to make a prior-year contribution after seeing your final income numbers, which matters for Roth IRA eligibility calculations.

The Epoch Times copyright © 2026. The views and opinions expressed are those of the authors. They are meant for general informational purposes only and should not be construed or interpreted as a recommendation or solicitation. The Epoch Times does not provide investment, tax, legal, financial planning, estate planning, or any other personal finance advice. The Epoch Times holds no liability for the accuracy or timeliness of the information provided.