Compared with China’s two state-owned rare-earth giants, U.S.-based companies seeking to bridge the gap between the two global superpowers still have a lot of catching up to do.

Some analysts attribute this lag to a historic lack of policy support and are hopeful that a substantial shift in this area will help narrow the divide.

According to the National Minerals Information Center at the U.S. Geological Survey (USGS), global rare earth mine production in 2024 was estimated to have increased to 390,000 tons, primarily driven by expanded mining and processing in China, Nigeria, and Thailand.

China alone produced 270,000 tons of rare earth minerals in 2024, a 5.9 percent increase from 255,000 tons in 2023. In comparison, the United States domestically produced about 45,000 tons of rare earth oxides in mineral concentrates, up by 9.7 percent from 41,600 tons in 2023.

Meanwhile, according to the International Energy Agency (IEA), China has a virtual monopoly on the extraction and refining of all rare earth magnets, controlling 61 percent of production and 92 percent of processing.

MP Materials, a U.S. firm that opened a magnet manufacturing facility in December 2024 in Texas, however, sees magnet manufacturing as the “most pronounced choke point” in U.S. rare earth production.

China produced an estimated 300,000 tons of NdFeB magnets in 2024, compared with MP Materials’ currently projected annual output capacity of about 1,000 tons, according to Rare Earth Exchanges, a data analytics platform for the rare earth industry.

The Far-Reaching Chinese Consolidation

Daniel O’Connor, CEO of Rare Earth Exchanges, a Salt Lake City-based rare earth technology platform, said the Chinese regime began playing a pivotal role in the global rare earth supply chain following the restructuring of the country’s fragmented industry into six major state-controlled entities, known as the Big Six.

According to a Congressional Research Service (CRS) report, China’s rare-earth production first began in the late 1950s in Inner Mongolia, in the northern part of the country. The Chinese regime made rare-earth development a top priority starting in the 1980s, leading to a significant increase in production during that period.

The former head of the Chinese regime, Deng Xiaoping, said at the time: “The Middle East has oil. China has rare earths.”

By the end of the 1990s, China had overtaken the United States and become a dominant, low-cost producer of rare earths.

In the early 2000s, China had a fragmented rare-earth industry with hundreds of producers, according to a paper published in the Journal of Resources and Ecology.

In May 2011, the Inner Mongolia government designated Baotou Steel Rare Earth High-Tech Co. as the sole government-controlled entity for mining and processing rare earth ore in northern China while ordering 31 private companies to shut down and four others to merge into Baotou Steel Rare. Later, the merged entity became known as the China Northern Rare Earth Group, according to the CRS report.

By 2016, hundreds of rare earth companies in southern China had been consolidated into five—Xiamen Tungsten, Minmetals Rare Earth, Guangdong Rare Earth, Aluminium Corp. of China (Chinalco), and China Southern Rare Earth, according to Strategic Metals Invest. Together with the China Northern Rare Earth Group, China’s rare earth “Big Six” came into being.

Through those Big Six companies, O’Connor said, China’s rare earth industry is vertically integrated, covering mining, refining, and downstream applications.

“It’s been a multi-decade, multi-phase program to dominate the world. But they didn’t just develop a monopoly upstream with access to the mines, they developed, importantly, monopolistic activity … in the midstream and processing and refining,” he said. “And so, what they’ve done over the last couple of decades is really perfect. They’ve turned the refining into a big, big business, and then downstream, they integrated with magnet production, which is what you need for defense or the automobile sector.”

However, the country’s consolidation of the rare earth industry didn’t end there. In December 2021, three of the “Big Six”—Aluminium Corp. of China, Minmetals Rare Earth, and China Southern Rare Earth—merged to become China Rare Earth Group.

In February 2024, only two companies—China Northern Rare Earth Group in the north and China Rare Earth Group in the south—were listed in Beijing’s new production quotas, establishing a two-giant industry structure, according to the CRS report.

This consolidation has transformed China’s rare-earth industry into a tightly controlled strategic asset, Felix Chang, a senior fellow at the Foreign Policy Research Institute’s Asia Program in Philadelphia, told The Epoch Times.

“On the one hand, such consolidation has enabled China to exert greater oversight and environmental control,” Chang said.

On the other hand, it has enabled the Chinese regime to implement export restrictions in 2024, he said, “precipitating global supply disruptions and highlighting China’s commanding position in the rare earths market.”

Chang said that while China’s upstream consolidation is largely complete, the downstream magnet manufacturing sector remains fragmented. He expects consolidation in that sector to accelerate.

From Leading to Catching Up

U.S. rare earth production did not begin until after the Molybdenum Corp. of America—which later changed its name to Molycorp Inc.—acquired most of the Mountain Pass mining claims and started small-scale production in 1952, according to the MP Materials website.

From the 1960s to the 1980s, the United States, specifically the Mountain Pass mine in San Bernardino County, California, was the world’s leading producer of rare earth elements, a USGS report shows.

However, the mine halted operation from 2002 to 2012 because of low rare-earth prices and environmental permitting issues in the United States, according to another USGS report.

According to the MP Materials website, the then-Molycorp encountered “significant challenges” and faced underinvestment at the time.

“As globalization reshapes the economy, attention on the rare earth industry wanes, allowing production to shift overseas,” the website reads.

The USCS report states that production moved almost entirely to China.

In 2010, China cut its rare-earth exports to Japan because of a months-long dispute between the two countries, raising concerns among many members of the U.S. Congress.

In 2012, Molycorp reopened the Mountain Pass mine. However, the company unexpectedly filed for Chapter 11 bankruptcy in 2015 with $1.4 billion in outstanding bond debt. The mine was again closed and remained shut for nearly two years, leading to the complete halt of all U.S. rare earth production in 2016 and 2017.

In 2017, Mountain Pass regained momentum after a new entity called MP Mine Operations (MPMO) purchased the mine. MPMO later merged with special purpose acquisition company Fortress Value Acquisition Corp. (FVAC), and in November 2020, FVAC changed its name to MP Materials Corp.

The deal raised $545 million and placed the firm on a path to becoming the nation’s only fully integrated rare earths company.

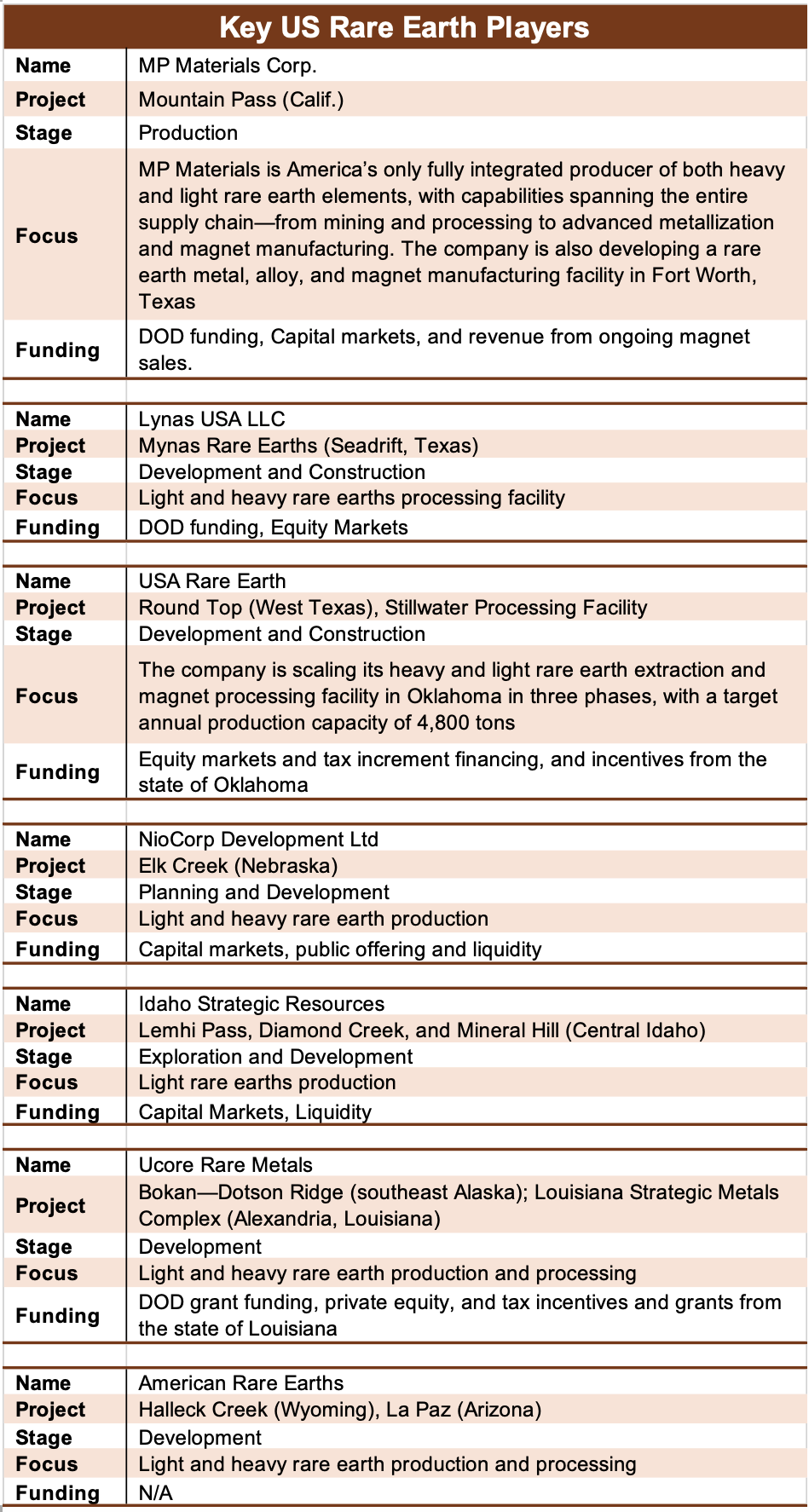

Other key players in the industry, including Lynas USA, USA Rare Earth, NioCorp Development, Idaho Strategic Resources, Ucore Rare Metals, and American Rare Earths, as listed by industry intelligence outlet Rare Earth Exchanges for The Epoch Times, have projects that remain in development or pilot stages and have yet to commence production.

DOD Investment Initiative

Although the U.S. Department of Defense (DOD) had invested in the emerging industry for several years under President Joe Biden, O’Connor said it was not focused enough. Since 2020, the DOD’s Manufacturing Capability Expansion and Investment Initiative (MCEII) has deployed a five-year rare-earth investment strategy to develop “mine-to-magnet” domestic capacity at all critical points of the rare-earth supply chain by 2027.

According to the DOD, the MCEII program has awarded more than $439 million to establish a domestic supply chain for rare earth elements, including the separation and refining of minerals mined in the United States, as well as the development of downstream processes to convert those refined materials into metals and then magnets.

Defense Secretary Pete Hegseth said recently that the Trump administration is currently conducting a review of the MCEII and all 72 active major defense acquisition programs.

“We’re establishing a new munitions war room, investing in expanding critical mineral production, including rare earth elements, heavy rare earth elements, light rare earth elements, all the things we need that need to be made at home or by our allies and partners,” Hegseth said on April 23 during remarks at the Army War College.

MP Materials received $45 million in DOD startup funds in early 2022 to design and build a facility for processing heavy rare earth elements (HREE) at the Mountain Pass production site.

Matt Sloustcher, the company’s chief communications officer, told The Epoch Times that since then, the company has invested more than $1 billion to bring its Mountain Pass mine and processing facility in California’s Mojave Desert online in 2023. In 2024, the Mountain Pass mine achieved record-breaking production, delivering more than 45,000 metric tons of rare earth oxides—an all-time high for U.S. primary production.

Besides MP Materials, the DOD has a similar agreement with Australia’s Lynas Rare Earths to establish another commercial heavy rare earths (HRE) separation facility in Seadrift, Texas.

After submitting technical capability plans to the DOD in 2022, Lynas USA has received $258 million from the department to locate both heavy and light rare earths facilities at the Texas site by 2026, along with potential future opportunities such as downstream processing and recycling, creating a circular mine-to-magnet supply chain.

Over the past year, however, Lynas has remained silent about the progress of the Texas facility. During an April 28 earnings briefing, Lynas CEO Amanda Lacaze informed analysts that the company’s U.S.-based rare earth project is costing more than initially expected and will require additional investment from the DOD.

“With respect to the U.S. facility, it is much more expensive because it is a greenfield facility. We talked about varying capacities there, and we continue to have a conversation with the U.S. government about really what is essential to [and] what is essential for the U.S. market and particularly for defense applications and ways that we can do that within sort of the regulatory environment in the U.S.,” she said.

Although some progress has been made with DOD and Department of Energy funding of processing facilities and magnet production pilot plants, Avadh Nagaralawala, a mining automation and control engineering consultant, told The Epoch Times that commercial-scale separation, purification, and magnet manufacturing, particularly for heavy rare earth elements (HREEs), are still not fully operational in the United States.

To accelerate that progress, O’Connor and Nagaralawala emphasized that the United States needs to close the remaining critical gaps in refining infrastructure, skilled labor, and lagging equipment and technology advancements.

If pilot plants transition smoothly to commercial operations and permitting reform accelerates, full-spectrum independence, including HREE separation and high-pressure magnet manufacturing, might take about 10 to 12 years without accelerated innovation and scale-up efforts, according to Nagaralawala.

“What’s needed is not just mining—but end-to-end capability. Until we build vertically integrated facilities that refine, separate, and manufacture rare earth components here at home, we’ll be reacting instead of leading,” he said.

On July 10, MP Materials announced a multibillion-dollar partnership with the Department of Defense and plans to build its second magnet manufacturing facility in the United States. The facility is expected to begin commissioning in 2028 and will have a projected production capacity of 10,000 metric tons.

The company called the partnership “transformational” for America’s rare-earth magnet independence.

Friends Read Free

Copy

Facebook

Tweet

Friends Read Free

Copy

Facebook

Tweet