Commentary

Medicare is not merely a senior health program; it is an elaborate intergenerational contract with a hidden clause: It quietly runs on a tax structure that is dependent on the birth rates among current workers. And that structure is crumbling.

The United States is facing a birth rate crisis. Fertility levels have fallen below the replacement rate, leading to an aging population and fewer workers to support it. This isn’t just a statistical anomaly—it’s a ticking time bomb for Medicare’s sustainability, access to care, and overall fiscal health.

The problem with the intergenerational transfer of wealth is that there isn’t going to be enough wealth to transfer.

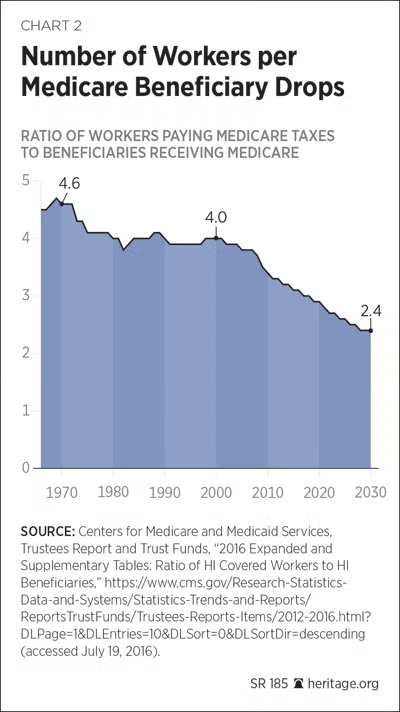

Medicare, enacted in 1965, was designed for a different era—one with higher birth rates and a robust worker-to-retiree ratio. The worker-to-beneficiary ratio has already fallen to 2.8-to-one today from roughly 4.2-to-one in the program’s early decades and is projected to reach 2.2-to-one by 2099.

Medicare Part A (Hospital Insurance) operates on a classic pay-as-you-go basis. Current workers and their employers remit a combined 2.9 percent Federal Insurance Contribution Act tax (as well as the 0.9 percent Additional Medicare Tax on high earners) into the HI Trust Fund. Those revenues immediately pay current claims rather than being saved and invested for future liabilities. The 2025 Medicare Trustees Report projects HI trust fund depletion in 2033—three years earlier than the prior estimate—after which incoming payroll taxes and premiums will cover only 89 percent of scheduled benefits.

The long-range actuarial deficit stands at negative 0.42 percent of taxable payroll, with a 75-year unfunded obligation of $3.1 trillion. Parts B and D, financed by general revenues and beneficiary premiums, are “solvent” only because Congress automatically appropriates whatever general funds are required; they already consume a rising share of the federal budget and trigger the Medicare funding warning for the ninth consecutive year.

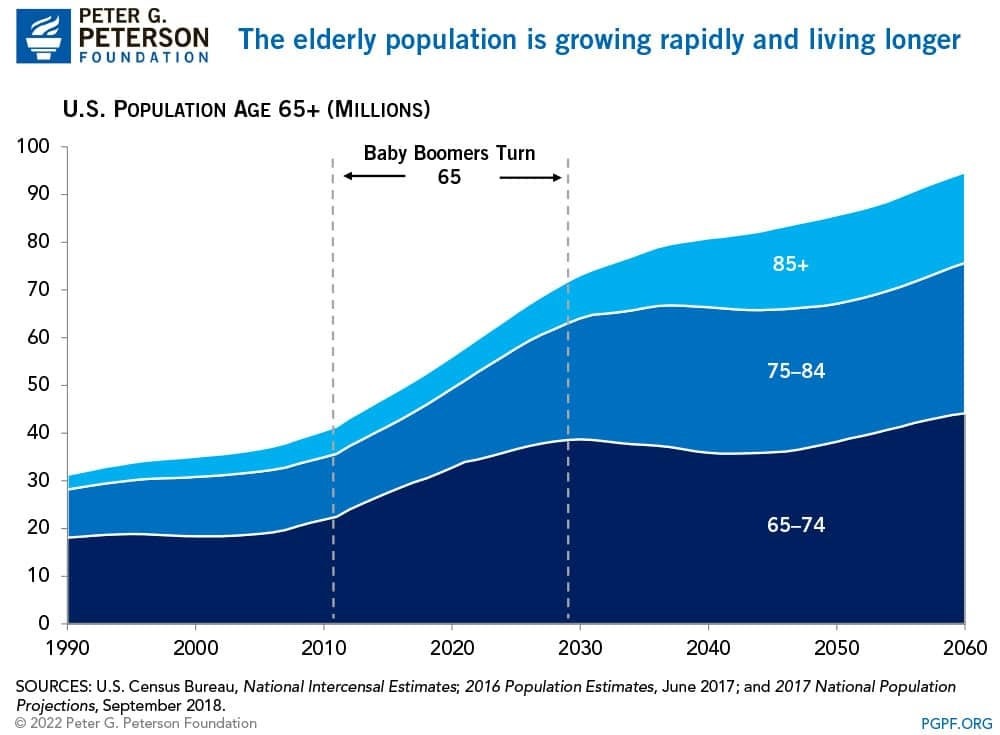

The U.S. fertility rate has dipped to about 1.6 births per woman, well below the 2.1 needed to maintain a stable population without immigration. This decline, accelerated since the Great Recession, shows no signs of reversal. According to the Centers for Disease Control and Prevention (CDC), birth rates hit a historic low in recent years, influenced by economic pressures, delayed marriages, and changing social norms. Meanwhile, life expectancies are rising, thanks to advances in medicine—better treatments for heart disease, cancer, and neurological conditions such as those I treat daily. The result? An unprecedented aging boom.

Today, 12 percent of Americans are 65 or older; by 2080, that could climb to 23 percent. This demographic math is unforgiving.

The 2025 Trustees Report explicitly ties this trajectory to the aging of the baby boom, slower labor-force growth, and an assumed ultimate total fertility rate of 1.9 children per woman. Actual U.S. fertility has undershot that assumption for years. Again, CDC data show the total fertility rate at 1.63 in 2024 and continuing to hover near historic lows in 2025. Each sustained tenth-of-a-point decline in fertility materially widens the long-term shortfall because it permanently reduces the future tax base relative to the retiree population.

With fewer workers contributing taxes, revenues can’t keep pace with escalating costs. Medicare spending, currently at about 3 percent to 4 percent of gross domestic product (with total national health expenditures at 18 percent of gross domestic product in recent data), could rise significantly in the coming decades, driven by more enrollees and rising per-person expenses from chronic conditions such as diabetes and obesity, which are prevalent in aging cohorts. Policymakers face tough choices: raise payroll taxes, cut benefits, or increase the retirement age. Higher taxes could burden younger generations already grappling with student debt and housing costs, potentially exacerbating the very fertility decline causing the problem.

Immigration offers a potential pragmatic solution. Increasing net immigration could offset much of the fiscal strain on Medicare and Social Security, bolstering the worker pool. Immigrants often arrive in active working years, contributing taxes without immediate benefit draws. Yet political debates and pragmatic realities make this approach difficult.

Countries such as Sweden and Norway offer cautionary tales.

In Sweden, immigration drove the majority of the country’s roughly 20 percent population growth since 1995 (to more than 10.4 million by 2021), contributing to persistent challenges including staff shortages, bed overcrowding, and long waiting times—29 percent of patients exceeded the three-month guarantee for a first specialist visit and 46 percent for treatment or surgery in 2021—while chronic conditions (affecting 82 percent of those aged 65 and older) account for 80 percent to 85 percent of total costs.

A free-market solution is ideologically straightforward but practically difficult. Medicare’s design creates classic third-party-payer distortions at the macro level. Workers face a compulsory intergenerational transfer whose return depends on future fertility and labor-force participation—variables they cannot control and that the program itself indirectly helps suppress.

In a genuine insurance market, individuals would purchase actuarially fair coverage for longevity and health risks, save in portable tax-deferred accounts, and face transparent prices for services. Competition among insurers and providers would drive innovation in both cost control and benefit design.

Reform must therefore link benefits more closely to individual workers.

Modernize Medicare’s benefit and financing structure. Convert the HI component to a premium-support model with risk-adjusted vouchers, allowing beneficiaries to choose among competing private plans. Gradually raise the eligibility age in line with gains in healthy life expectancy. Introduce meaningful means-testing for supplemental subsidies. These steps reduce the unfunded liability, improve price signals, and lessen the tax burden on working-age Americans.

Second—and admittedly more difficult—policymakers must address the fertility side of the ledger directly. Empirical evidence suggests modest, targeted tax incentives yield better results than broad entitlements, which often fail to durably lift fertility amid deeper cultural shifts toward delayed parenthood. For instance, studies of child tax credits and similar financial supports show positive but limited effects on birth probabilities, with elasticities typically in the 0.05 to 0.41 range (say, increasing benefits by 10 percent of household income is linked to 0.5 percent to 4.1 percent higher birth rates). This framework respects individual liberty, rewards responsibility, and sustains civilization through voluntary family formation rather than top-down engineering.

None of this requires utopian assumptions about birth-rate engineering. Markets do not guarantee any particular fertility level, but they do minimize artificial penalties on the decision to have children. By contrast, the status quo imposes a hidden fertility tax: Extract resources from young adults, promise them future benefits whose value erodes with every successive actuarial revision, and then express surprise when cohort fertility remains below replacement.

Declining birth rates are not merely a demographic curiosity—they are a direct threat to Medicare’s viability. The free market offers solutions.

From the American Institute for Economic Research

Views expressed in this article are the opinions of the author and do not necessarily reflect the views of The Epoch Times.

Friends Read Free

Copy

Facebook

Tweet

Friends Read Free

Copy

Facebook

Tweet