New Zealand’s government spent $66 billion responding to COVID-19—$16 billion more than originally announced—much of it in ways Treasury now says were unnecessary and difficult to unwind.

A new Treasury report says the scale of discretionary spending was among the largest globally and left structural deficits that will burden future governments. It also warns against relying on outdated crisis responses and calls for clearer fiscal rules to prepare for future economic shocks.

In 2020, the Labour-led coalition government (which included the Greens and NZ First) announced a $50 billion COVID-19 response package.

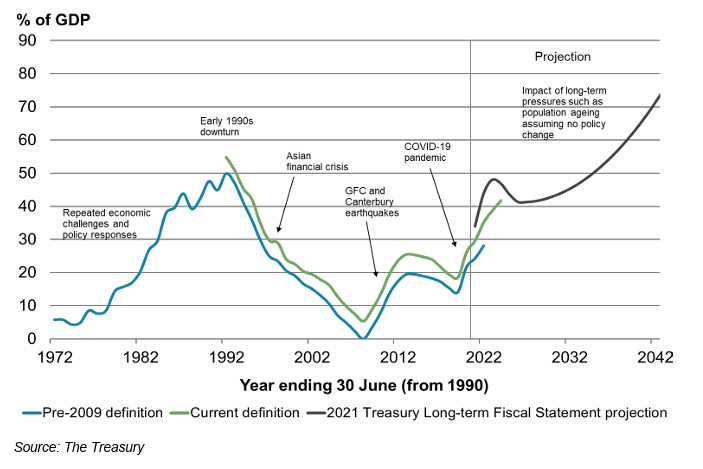

Treasury now reveals that the final bill came in much higher, equivalent to around 20 percent of the country’s GDP.

“The International Monetary Fund and Organisation for Economic Co-operation and Development (OECD) estimated it to be among the largest COVID-19 responses globally,” the report states.

Around half of the spending was tied directly to the pandemic, such as health measures and the Wage Subsidy Scheme.

However, a “significant component” of the funding later shifted toward other goals, like economic redistribution, raising concerns within Treasury about fiscal discipline.

Initially, Treasury supported prioritising economic recovery over budget constraints. But as the economy recovered by late 2020 and into 2021, it advised a shift towards more targeted support.

By Budget 2022, officials were urging the government to stop additional stimulus spending.

That advice was ignored.

“Changing economic conditions … led to downward revisions to forecasts for revenue and expenditure,” Treasury noted, adding that structural deficits began to emerge after 2021.

Some of the government’s programmes, packaged under the COVID-19 umbrella, had only loose connections to the pandemic and proved hard to phase out.

“The combination of these factors meant that the fiscal impact of the COVID-19 response was much larger than expected,” Treasury added.

The paper also examines policies employed to address other major events, such as the 2023 North Island weather disasters, the Canterbury and Kaikōura earthquakes, and the 2008 global financial crisis (GFC).

It concludes that governments have repeatedly failed to build financial buffers during good times, leaving future generations exposed.

Looking ahead, Treasury urges policymakers not to assume that the next large shock will be similar to previous ones.

“Historical information offers some guidance to the future,” it said.

“But relying too heavily on it carries the risk of policy responses ‘fighting the last war.'”

It also warns that public expectations of government bailouts during crises may reduce private risk management, weakening societal resilience.

“The expectation that governments will provide support to soften the direct impacts of shocks can reduce the incentives for firms, households, and communities to manage their own risks,” Treasury warned.

“This could reduce society’s overall resilience [and] increase the cost of shocks to governments.”

To counter this, Treasury recommends pre-defined, cross-party agreements on how fiscal policy should respond to different types of shocks.

“Being prepared would allow faster responses and improved targeting and could ensure better value for money,” it said.

While Keynesian stimulus—such as investing in infrastructure—has traditionally been used to soften the economic blow of downturns, Treasury now calls this approach “less effective” due to slow rollouts.

“There are long lags between investment decisions and construction activity,” Treasury said.

“Adjusting the scale of maintenance and repairs could be a more timely option. Ongoing fiscal consolidation [will be needed], implying difficult trade-offs for future governments.”

Friends Read Free

Copy

Facebook

Tweet

Friends Read Free

Copy

Facebook

Tweet