Accurate information on the jobs market and inflation is critical for U.S. policymakers; it’s the core mission of the Bureau of Labor Statistics (BLS). In recent years, the bureau has faced scrutiny over claims that its jobs data may be unreliable and biased.

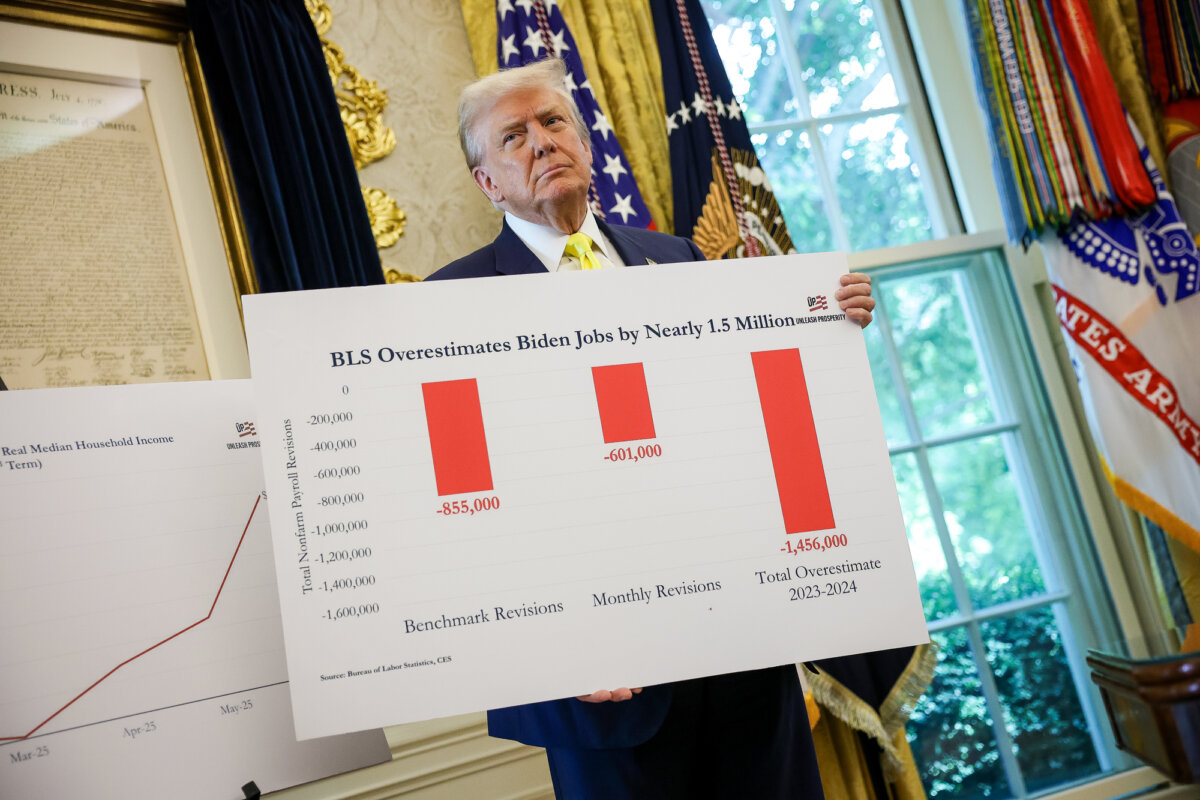

That pressure intensified on Sept. 9 when the BLS issued its largest-ever revision, retroactively lowering jobs growth by 911,000 for the 12 months that ended in March 2025.

The Trump administration criticized the revision, which shows that the U.S. economy added nearly 76,000 fewer jobs per month than first reported, mostly under the Biden administration.

“President [Donald] Trump was right: Biden’s economy was a disaster and the BLS is broken,” White House press secretary Karoline Leavitt said in a Sept. 9 statement.

On the same day, Trump posted on Truth Social, quoting Jay Hatfield, CEO of Infrastructure Capital Advisors, who told Fox Business: “The entire organization is broken. It needs to be fixed. They need to use modern sources of information.”

Hatfield said that if the Fed had “followed what we published, they would have raised rates in early 2021.”

The BLS plays an important role in shaping the Federal Reserve’s monetary policies, as its monthly reports on payroll growth, unemployment, and wages feed directly into the central bank’s view of the labor market. Strong employment data can prompt the Fed to raise interest rates to rein in inflation, while weak numbers may lead to rate cuts aimed at stimulating economic growth.

Because these decisions directly affect borrowing costs for households and businesses, from mortgages and auto loans to business financing, the accuracy and credibility of BLS data are essential, according to experts. Problems in data not only risk misleading policymakers but can also disrupt markets and impact economic activity.

The revisions are happening because the methods used by the BLS for estimating job growth are outdated, according to Sean Higgins, a research fellow at the Competitive Enterprise Institute specializing in labor and employment issues.

“It’s mostly almost like an analog level system where they just send out surveys to businesses and wait till the surveys trickle back in,” Higgins told The Epoch Times.

BLS also has staff in the field who conduct statistical samples, he noted, visiting businesses to ask about payrolls and monthly performance.

“That’s not necessarily bad information, but it is a sort of definitive number for the entire economy,” he said.

Trump began voicing his frustration with the BLS on Aug. 1, when the agency announced that the U.S. economy added just 73,000 jobs in July, well below economists’ expectations. The announcement also included downward revisions of 253,000 jobs for the months of May and June.

Trump suggested that the employment numbers were “manipulated for political purposes.”

“I was just informed that our Country’s ‘Jobs Numbers’ are being produced by a Biden Appointee, Dr. Erika McEntarfer, the Commissioner of Labor Statistics, who faked the Jobs Numbers before the Election to try and boost Kamala’s chances of Victory,” he wrote on Aug. 1 on Truth Social.

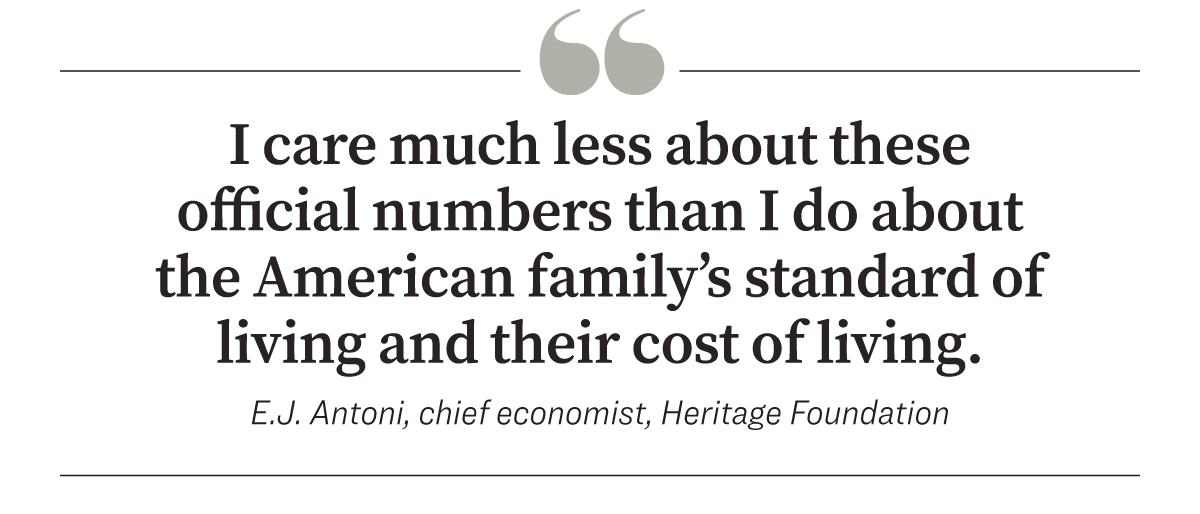

Trump then removed McEntarfer from her role and nominated E.J. Antoni, chief economist at The Heritage Foundation and a longtime critic of the agency, to lead the BLS.

“I care much less about these official numbers than I do about the American family’s standard of living and their cost of living,” Antoni told Jan Jekielek, host of “American Thought Leaders,” in a June interview.

“Don’t pay so much attention to what the government is telling you the official numbers say. Pay more attention to your personal pocketbook because at the end of the day, that’s what really matters.”

How BLS Conducts Surveys

The BLS, part of the Department of Labor, is responsible for publishing a range of data on the labor market, prices, and productivity. In addition to labor statistics, the federal agency also issues key inflation reports, including the Consumer Price Index (CPI) and Producer Price Index (PPI).

The agency collects data from both private and public entities and releases its monthly nonfarm payroll report, formally called the Employment Situation Summary, at 8:30 a.m. Eastern Time on the first Friday of each month.

The report is based on two major data sources: the establishment survey and the household survey.

The establishment survey, or the Current Employment Statistics (CES), provides data on employment, average weekly hours, and hourly earnings by sector. It is a survey of approximately 121,000 businesses and government agencies tracking more than 630,000 nonfarm work locations.

The monthly household survey, or the Current Population Survey (CPS), interviews about 60,000 households to obtain information about the unemployment rate, labor force participation, and types of employment, such as full-time, part-time, and self-employed.

Both surveys are conducted through a mix of telephone, email, and mail.

Bureau officials then review the data to spot processing errors, clarify information, and report discrepancies. After the raw data is processed, the federal agency considers other factors, including seasonal hiring trends and adjustments.

The monthly report presents employment numbers for the prior month along with revisions to previously released job numbers.

Higgins explained that delays in receiving survey data and other adjustments are slowing down the process. Hence, people have good reason to wonder if the monthly numbers are accurate and reliable, he said.

Still, he believes that the revisions are not politically motivated; he said collecting the monthly data is “a staggeringly difficult job.”

“A lot of these companies just simply go out of business, and new ones emerge. And keeping track of that and adjusting for that factor is very difficult,” Higgins said.

And there are also nontraditional jobs in the gig economy, such as driving for Uber or Lyft, he noted.

Large Data Discrepancies

While substantial discrepancies have appeared periodically over the years, the most significant and persistent revisions that garnered widespread attention began during and after the COVID-19 pandemic.

At the onset of the pandemic, the BLS reported enormous volatility in the employment data due to massive job losses followed by swift rebounds. Many initial figures were later revised as delayed survey responses from businesses gradually arrived, reflecting the challenges of capturing real-time labor market shifts during a period of economic upheaval.

To present a more accurate picture of employment conditions, the bureau publishes the annual preliminary benchmark revisions.

For 90 years, the bureau has conducted annual benchmark revisions, depending on more comprehensive datasets to generate accurate labor trends. Over the past three decades, officials have compared the monthly jobs data to the Quarterly Census of Employment and Wages (QCEW), which consists of quarterly unemployment insurance tax filings.

The latest report confirmed that U.S. job growth was overstated by 911,000 jobs from April 2024 to March. This represented a 37 percent decline from the federal agency’s initial estimate of 2.4 million new jobs and accounted for a 0.6 percent share of overall employment—the 10-year average is 0.2 percent.

The BLS attributed “response error and nonresponse error” to the overestimated employment growth.

“First, businesses reported less employment to the QCEW than they reported to the CES survey (response error),” the bureau stated. “Second, businesses who were selected for the CES survey but did not respond reported less employment to the QCEW than those businesses who did respond to the CES survey (nonresponse error).”

A key challenge for the bureau has been declining response rates. Since April 2015, the response rate has declined to about 43 percent from 61 percent.

Similar revisions have been showcased in previous years.

From April 2023 to March 2024, the bureau lowered employment growth by 818,000, or 30 percent. For the period from April 2022 to March 2023, officials found 306,000 fewer jobs than initially reported.

Calls to Modernize BLS

Shortly after the preliminary benchmark revisions were released, Labor Secretary Lori Chavez-DeRemer issued a statement pledging to find a solution by modernizing the data collection system.

“Considering these reports are the foundation of economic forecasts and major policy decisions, there is no room for such a significant and consistent amount of error,” she said.

“Leaders at the bureau failed to improve their practices during the Biden administration, utilizing outdated methods that rendered a once reliable system completely ineffective and calling into question the motivation behind their inaction.”

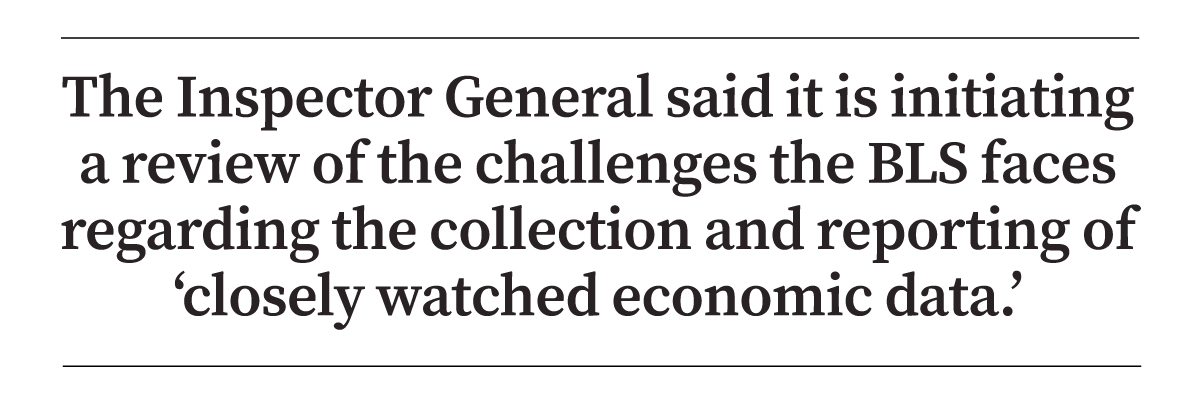

The Department of Labor’s internal watchdog confirmed in a Sept. 10 letter that the Office of the Inspector General is initiating a review of the “challenges” the BLS faces regarding the collection and reporting of “closely watched economic data,” including inflation and jobs.

Nancy Tengler, CEO of Laffer Tengler Investments, agreed that calculating national employment is difficult, but it still calls into question “the reliability of all the other numbers.”

“The process is, to say the least, fraught,” she told The Epoch Times in an email.

Rep. Jason Smith (R-Mo.), chair of the House Ways and Means Committee, argued that Americans are struggling with high interest rates because the Fed relied on overstated jobs data.

“If the Federal Reserve has been basing interest rate decisions on preliminary data from the Bureau of Labor Statistics, then American families who’ve suffered under high rates deserve a massive correction by the Fed as well,” he said in a Sept. 12 statement.

Policy Implications for the Fed

When the U.S. central bank paused its easing cycle in January after three consecutive interest rate cuts, monetary policymakers defended the action by stating they could afford to be “patient” with rate cuts.

Since economic prospects were intact and the U.S. labor market remained solid, the Fed could wait before cutting interest rates again and assess how Trump’s tariffs were influencing the economy, particularly inflation.

“The labor work is solid; inflation is low. We can afford to be patient as things unfold. There’s no real cost to our waiting at this point,” Fed Chair Jerome Powell told reporters at a post-meeting press conference in May.

In a speech in June, Minneapolis Fed President Neel Kashkari said monetary policymakers were seeking more clarity from the administration’s sweeping trade agenda.

“The Federal Reserve has basically been in wait-and-see mode, saying we need to get more clarity on how this is all playing out in the economy before we are confident on what tariffs are going to do to inflation,” he said.

Some policymakers have warned about slowing job growth and called for rate cuts without further delay.

Since June, Federal Reserve board member Christopher Waller has suggested that it would be appropriate to change direction, pointing to the lack of tariff-driven inflation and deteriorating employment conditions.

“My final reason to favor a cut now is that while the labor market looks fine on the surface, once we account for expected data revisions, private-sector payroll growth is near stall speed, and other data suggest that the downside risks to the labor market have increased,” Waller said in an Aug. 1 statement defending his dissent at the July Federal Open Market Committee meeting.

According to Waller, the current data suggest that the policy rate should be at about 3 percent, rather than the current level, which is between 4.25 percent and 4.5 percent.

Dan Varroney, president and CEO of Potomac Core Consulting, said the Fed would have cut interest rates earlier had it known the initial job numbers were overstated.

“Yeah, absolutely,” Varroney, who is also author of the new book “Rethinking Economic Growth,” told The Epoch Times.

Varroney said the Fed policymakers waited 12 to 14 months to raise interest rates in 2022, and now they are waiting way too long to ease monetary policy.

The federal funds rate is a key policy rate that influences borrowing costs for businesses, consumers, and governments.

Data from the CME FedWatch Tool indicate that Wall Street overwhelmingly expects the Fed to lower rates by a quarter point from the current target at the next policy meeting on Sept. 16 and 17.

Powell, in his final keynote address at the central bank’s annual retreat in Jackson Hole, Wyoming, conveyed a pivot on monetary policy.

“The shifting balance of risks may warrant adjusting our policy stance,” Powell said on Aug. 22.

Varroney, echoing calls from the president and Treasury Secretary Scott Bessent, thinks the Fed needs to catch up and become more aggressive with rate cuts.

The futures market is currently expecting two more quarter-point rate cuts by the end of this year.

For months, Trump has urged Powell to lower interest rates, arguing that doing so would bolster the U.S. economy and save the federal government hundreds of billions of dollars per year in interest charges.

“Jerome ‘Too Late’ Powell should have lowered rates long ago. As usual, he’s ‘Too Late!’” the president said in a Truth Social post on Sept. 5, following the weak August jobs report, which shows that the economy added just 22,000 jobs compared to the previous month.

While Trump has confirmed he won’t terminate Powell before his term ends in May 2026, the administration is in the process of seeking his replacement.

Trump recently named his top three candidates for the role, including former Feb board member Kevin Warsh, current Fed board member Waller, and National Economic Council Director Kevin Hassett.

Trump has signaled that he wants to appoint someone who is more inclined to lower interest rates.

Friends Read Free

Copy

Facebook

Tweet

Friends Read Free

Copy

Facebook

Tweet