Commentary

Many signs are pointing to serious trouble in the private credit markets. Among many others, JPMorgan CEO Jamie Dimon has warned that private credit losses will be “larger than expected.” That’s a serious statement concerning a crucial financial segment often valued in excess of $15 trillion globally.

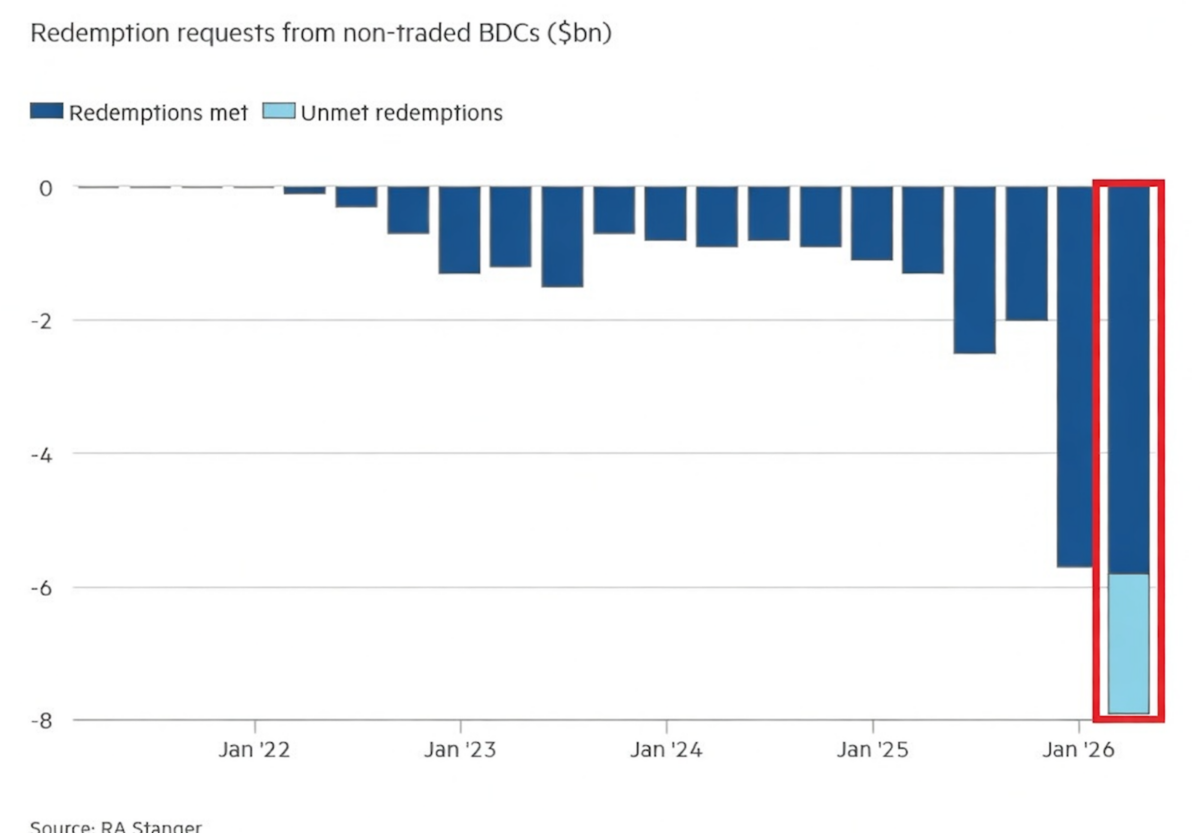

Demands of depositors for redemption now are growing, but many companies have throttled withdrawals, only increasing worry and intensifying demand. We aren’t yet at run levels of panic, but it is not clear when we would know that with certainty.

These companies have emerged over the decades as restrictions on investment have loosened, credit has been cheap, and investors looking for returns have banked on large wealth holdings to generate profits. Private credit has been a major force in industrial reorganization in many sectors, from entertainment to medicine to housing.

Private equity particularly targets industry with recurring revenue streams, with the hope of cutting costs, broadening the client base, and insisting on great adherence to the subscription mode.

It’s been comical if not cruel to watch as private equity companies have eaten up bowling alleys and run them with zero expertise in how to do so. It’s the same with mobile home parks, as managers and companies newly in charge deny services to paying customers and attempt to squeeze ever more homes in spots. In veterinary clinics, it means insisting on annual “wellness” checkups and mass consumption of shots and services, clearly exploiting every pet owner’s fears.

There is a scene in the movie “Wall Street” when Bud, the baggage claim summer intern, suddenly becomes CEO because he is tight with the moneybags tendering a takeover bid. He prattles on about new routes, new operations flows, cost savings, and new offerings without the slightest clue of what he is speaking. It’s this way very often with these companies.

Private equity itself has been the beneficiary of huge lending, which means that it has enormous leverage to service, putting ever more pressure on newly acquired firms to generate fabulous new revenue streams like magic. It’s worked, mostly, but the conditions why are not persistent.

A key to such investing is that depositors agree to restrictions on withdrawals in exchange for what they hope are high returns from the decisions of the fund managers. It’s not been an issue for years, as private equity has gobbled up countless numbers of businesses. Over the past year, it has become an issue.

Private credit funds are often backed by pension funds, insurance companies, endowments, and, increasingly, retail investors. They offered direct loans, often floating rate, to companies too small or too leveraged for public bond markets or traditional bank term loans.

In exchange, they demanded higher yields, typically a premium over public credit, along with customized contracts that allow borrowers to defer cash interest payments by issuing more debt. That’s right, it’s turtles all the way down for these deals.

Keep in mind the industrial effect of artificially low interest rates, i.e., those unsupported by existing capital and savings. They signal investors to move money toward longer-term projects, skewing the balance of the production structure and changing the market shape of the yield curve. That means redirecting resources in places that cannot be sustained once conditions change.

This model worked brilliantly in a low-interest-rate environment. Cheap credit fueled leveraged buyouts, corporate expansions, and consolidations. Private credit players such as Blackstone, Apollo, KKR, Ares, and Blue Owl became powerhouses. Returns often hit double digits, outpacing many public alternatives while promising an “illiquidity premium” for locking up capital for years.

Investors tolerated the restrictions—quarterly redemptions were often capped at 5 percent of net asset value—because assets performed and liquidity demands stayed low. Fund managers thrived on fees from assets under management growth.

The ground shifted with rising interest rates starting in 2022, a new policy undertaken to curb inflation. Higher borrowing costs squeezed highly leveraged borrowers, many of whom had loaded up on debt during the easy-money years. Defaults, while still below some historical peaks in headline figures, have climbed.

Private credit funds have heavy exposure to artificial intelligence companies—estimates put it at about 20 percent of some portfolios, with $500 billion in related lending. AI tools automating coding and other functions have eroded revenue models for many of these firms, leading to valuation writedowns.

One dramatic example involved a BlackRock private loan marked from 100 cents on the dollar to zero in just three months. As software borrowers faltered, fund valuations came under scrutiny, prompting investors to question whether reported returns reflected reality.

This uncertainty triggered a surge in redemption requests. In late 2025 and early 2026, requests spiked across major players. Blue Owl faced demands that led it to sell $1.4 billion in assets and eventually restrict quarterly redemptions.

Stock prices of public private credit managers reflected the stress: Blue Owl is down sharply (about 40 percent year-to-date), while Blackstone, KKR, Apollo, and others are off by 20 percent or more, contributing to a broader $265 billion wipeout in market cap for exposed firms.

Many funds remain closed-end with locked capital for five to 10 years, reducing run risk compared with open-end structures. Defenders argue that this is a recalibration, not a crisis: a “wake-up call” testing liquidity provisions that were always disclosed, with redemption caps working as designed. We shall see, but conditions are also ripe for growing trouble.

Private credit has become integral to corporate finance, funding innovation, restructuring, and growth. A prolonged meltdown—rising defaults snowballing into forced asset sales, tighter credit availability, and valuation spirals—could constrain borrowing, wage growth, and job creation in affected sectors.

Entertainment, medicine, and housing, already reshaped by private capital, might face consolidation. Retail investors, drawn in by the search for yield in a low-rate world, could suffer losses or locked capital, eroding trust in alternative investments.

While not “too big to fail” like 2008 banks, the industry’s opacity—limited public disclosures, mark-to-model valuations, and complex interconnections—makes risks hard to quantify. Geopolitical tensions, policy uncertainty, and any recession would exacerbate this.

The cycle is testing a generation of managers who know nothing of tight-credit markets. Survivors could emerge stronger, with better risk pricing and structures. But the current strains signal that the easy era is over. What began as an innovative workaround for regulatory barriers now faces its first major stress test in a tightening environment.

What’s particularly sad to me is to see how many family-owned and privately held firms and retail shops have been demolished in this frenzy. There is no undoing this. Here we have a particularly destructive example of the poison of cheap credit—artificially subsidized by central bank policy—that can completely wreck the normal functioning of capitalism itself. Indeed, it is a tragedy with grave consequences for our lives.

Time could be running out for private credit and equity. The carnage from a full collapse could become crisis-level. The bigger lesson is what is generally not spoken: Authentic capitalism has no greater enemy than the cheap money enabled by a central bank. Here is a force that turns regular commerce—normally humane and socially wonderful—into a rapacious environment solely focused on survival.

Views expressed in this article are the opinions of the author and do not necessarily reflect the views of The Epoch Times.

Friends Read Free

Copy

Facebook

Tweet

Friends Read Free

Copy

Facebook

Tweet