Commentary

2026 arrived with the thundering arrest of former Venezuelan leader Nicolás Maduro.

In the first weeks, U.S.–European relations were rattled by an extraordinary standoff over Greenland, including threats of immediate tariffs on several European and NATO allies, before the White House later softened its stance and ruled out military action.

President Donald Trump threatened new tariffs on Canada, reopening questions about the stability of North American trade just as earlier tariff disputes remained unresolved.

At the same time, the Department of Justice served grand jury subpoenas to Federal Reserve Chairman Jerome Powell, an escalation without modern precedent that prompted rare public defenses of central bank independence from former Fed officials.

Markets reacted quickly. Amid geopolitical risk, policy credibility, a U.S. public debt crisis, and unresolved trade tensions, gold shot up by 17 percent year-to-date, briefly reaching $5,100 per ounce, and silver surged by more than 50 percent, shattering record after record, extending relentless gains following a volatile 2025.

Meanwhile, U.S. equities remained near record highs while cryptocurrency struggled to regain relevance. Beneath the surface, labor data softened. Unemployment ticked higher, and labor force participation remained low, while financing conditions continued to restrict interest-sensitive sectors.

These early movements prompt a key question: Do last year’s winning trades still apply in the market now taking shape?

Precious Metals: A Clear Winner That Refuses to Cool

Precious metals were among the top-performing asset classes of 2025. Gold posted a phenomenal return of more than 65 percent, platinum surged by 120 percent, and silver delivered an extraordinary return of about 170 percent. That momentum has only intensified in early 2026.

However, investors are no longer treating gold, silver, and platinum as a unified asset class. Each metal is now being driven by a distinct mix of demand, policy, and supply dynamics.

Gold: Safe-Haven Appeal With Structural Support

Gold’s rally is driven by multiple reinforcing factors rather than a single catalyst. Central banks remained persistent buyers throughout 2025, continuing a multiyear shift in reserve composition—even as gold prices rose. This reflects diversification away from the U.S. dollar, heightened geopolitical risks, and inflation hedging strategies.

In 2025, global official gold holdings surpassed U.S. Treasury securities as a share of central bank reserves for the first time in 30 years, and that lead has continued to widen.

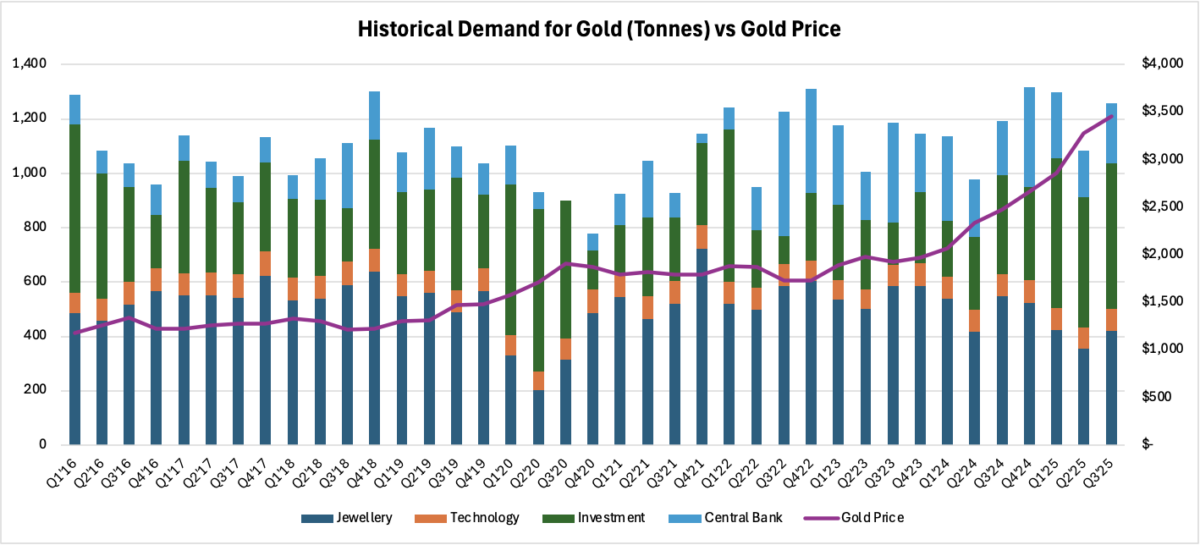

Data source: gold.org

Data source: gold.orgAs shown in the chart (up to the third quarter of 2025), investor behavior over the past decade has reinforced this trend. After nearly four years of net exchange-traded fund outflows, gold exchange-traded funds saw record inflows in 2025, tightening financial supply and supporting prices. Jewelry demand, particularly in India and China, proved more resilient than expected despite high prices—suggesting that demand is being deferred, not destroyed.

On the supply side, gold production remains structurally constrained. Mine output grows slowly, recycling responds with long lags, and new supply cannot scale quickly. Thus, price movement primarily reflects allocation shifts rather than changes in physical availability.

Interest rates remain a supportive factor. With Powell’s term ending in May, his successor may pursue a more dovish stance. High public debt levels also limit the scope for aggressive tightening. A renewed push toward monetary easing could further fuel the rally.

If risk and uncertainty persist, it may not be too late to participate. Gold offers defensive positioning with at least modest upside.

Silver: Industrial Demand Meets Policy Friction

Silver’s rally has been sharper and more volatile than gold’s, owing to its dual role as a monetary and industrial metal.

Industrial demand remained strong through 2025, supported by solar deployment, electrification, grid expansion, and data center infrastructure—none of which showed signs of slowing in early 2026.

Policy developments have added friction. China, which refines a significant share of global silver, introduced tighter export licensing requirements beginning in 2026, further tightening physical markets.

Meanwhile, India elevated silver’s formal monetary role. Effective on April 1, 2026, India’s central bank began allowing silver jewelry and coins as collateral, bringing silver closer to gold in regulatory status.

In addition, the U.S. Department of the Interior officially added silver to its list of critical minerals in November 2025. This underscores silver’s vital role in national security, technology, and manufacturing.

Despite soaring prices, silver supply remains constrained. Unlike gold, silver is often consumed rather than stored, and the resulting structural deficit is expected to continue after five consecutive years, driven by both industrial and investor demand.

Compared with gold, silver’s market is smaller and more volatile. The annual value of silver production is a fraction of gold’s, making it more sensitive to shifts in policy and investment. Although volatility will remain, the scale of silver’s recent gains may be difficult to sustain.

Platinum: The Dark Horse

Since late 2024, platinum has risen by more than 150 percent, driven by a different set of forces and marked by unique uncertainties.

Supply remains tight and geographically concentrated. Demand is cyclical and sensitive to substitution, varying across automotive catalysts, chemical processing, and glass manufacturing. After years of underperformance, platinum reentered investor focus in late 2025 as capital rotated toward less crowded precious metal exposures.

The World Platinum Investment Council forecasts a narrow surplus in 2026 and a deficit from 2027 to 2030.

Platinum lacks gold’s monetary premium and silver’s broad industrial base, making it the most speculative of the three metals—but also the most reactive to investor sentiment.

AI: A Narrow Engine Carrying the Equity Market

Artificial intelligence (AI) defined equity markets in 2025 and remains a dominant force in early 2026. However, its influence has become increasingly concentrated.

U.S. equities posted strong headline returns in 2025, but gains were uneven. Nvidia and Alphabet alone accounted for a disproportionate share of the S&P 500’s total return. Equal-weight indices and non-AI sectors lagged notably.

Sustaining AI growth requires massive investment. At the center is a capital-intensive loop: Model developers depend on vast computing power, cloud providers fund and operate infrastructure, and chipmakers build the hardware. A December 2025 CNBC review compared the scale of this investment to past telecom and energy buildouts, raising concerns about leverage and return on capital.

A market led by a handful of companies remains vulnerable to shifts in financing, policy, or expectations regarding AI monetization. Meanwhile, productivity gains are uncertain. McKinsey’s “The State of AI in 2025” report found that although AI adoption is rising, measurable productivity improvements remain limited. A similar conclusion was reached in MIT’s “The ‘Productivity Paradox’ of AI Adoption in Manufacturing Firms,” which states that gains often lag because of integration costs and organizational disruption.

Capital continues to flow into AI-linked companies, while the broader market remains range-bound. Outside of AI, the real economy tells a more restrained story. According to the Bureau of Labor Statistics, job growth has slowed, labor force participation remains low, and unemployment has edged up. Gains are concentrated in health care and government, while cyclical sectors remain weak.

Markets are pricing continued dominance by a narrow group of companies with intact earnings stories, but this concentration raises the stakes should confidence waver.

Crypto: Digital, but Not Gold

Despite being marketed as “digital gold,” cryptocurrencies underperformed during times of crisis when traditional safe-haven assets surged. Bitcoin and other tokens delivered volatile but ultimately lackluster returns relative to gold and silver, particularly during periods of geopolitical tension and policy uncertainty.

Rather than acting as a hedge, crypto often moved in tandem with U.S. tech stocks, showing high sensitivity to liquidity and policy signals. The GENIUS Act centralized parts of the ecosystem by regulating dollar-backed stablecoins, thereby undermining claims of decentralization.

Liquidity remains highly concentrated among a few exchanges, custodians, and issuers, making crypto vulnerable to regulatory scrutiny, enforcement actions, and monetary policy. Enforcement cases and scams continued to erode trust, especially among retail users.

In 2025, crypto failed to deliver as a haven. In 2026, it continues to struggle to establish relevance beyond being a speculative asset.

Rates, Bonds, and Real Estate: Relief With Constraints

After a period of aggressive rate hikes, the Federal Reserve pivoted in 2025, cutting interest rates by a total of 75 basis points. Additional cuts are expected in 2026.

As a result, long-term interest rates fell, with 30-year fixed mortgages dropping to about 6.09 percent from nearly 7 percent by late January 2026. Still, financing conditions remain tight. Lenders are cautious, and underwriting standards are restrictive. Residential real estate faces affordability and supply constraints, while commercial real estate remains under pressure.

With yields stabilizing, bonds regained some utility in 2025. However, record Treasury issuance continued to pressure term premiums, limiting the decline in yields. Concerns about fiscal priorities and central bank independence added noise to the long end of the yield curve.

In 2026, bonds are likely to continue recovering their portfolio role—but aggressive reallocations remain unlikely.

2026: A Year Full of Dynamics

Markets in 2026 are responding to diverse and often conflicting pressures. Growth is slowing, but not collapsing. Inflation is easing, but not disappearing. Tariff tensions remain unresolved. Some policies are supportive; others are constrained.

Capital continues to move, but with greater selectivity and lower tolerance for disappointment. Markets appear less willing to embrace simple narratives. Although 2025 rewarded a narrow set of AI-linked stocks, 2026 may increasingly favor assets tied to structural themes—monetary credibility, resource control, and capital intensity—while punishing those that rely purely on confidence.

For now, precious metals are shining. The message from markets isn’t clarity—it’s caution. And that may be the most important signal of the year.

Views expressed in this article are the opinions of the author and do not necessarily reflect the views of The Epoch Times.

Friends Read Free

Copy

Facebook

Tweet

Friends Read Free

Copy

Facebook

Tweet