Commentary

Washington is buzzing with news of possible upheaval at the Federal Reserve. President Donald Trump has floated the idea of firing Chairman Jerome Powell on grounds that he is keeping interest rates too high. Wall Street is deeply concerned that such an action would compromise the Fed’s independence and put stable monetary policy at risk.

There is every reason to be dubious about Trump’s reasons for firing Powell. Lower rates would indeed risk kicking off a second wave of inflation, not immediately but within a year or two. We barely shook off the last bout that began with zero percent rates in 2020 most immediately but truly tracing back to the Fed’s misbegotten response to the 2008 housing crisis.

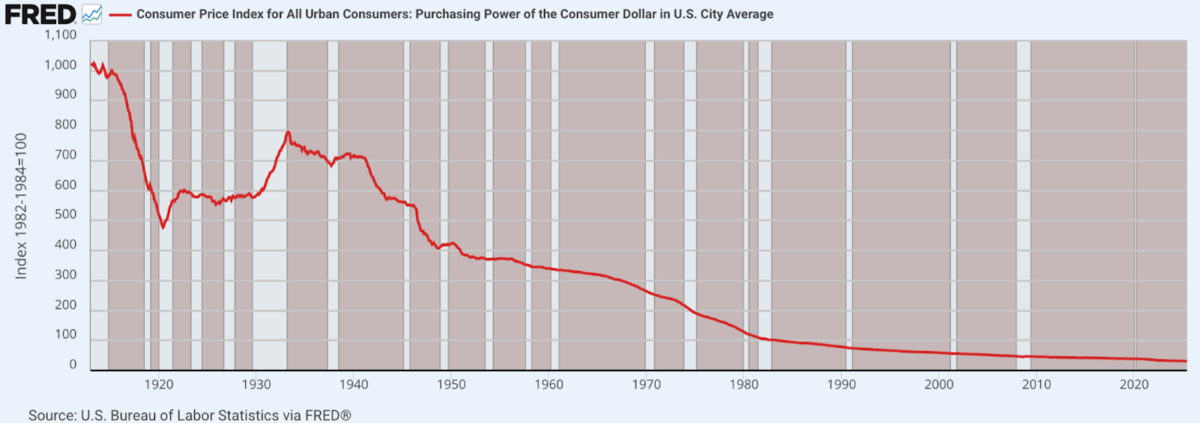

The trouble with the critique concerning the Fed’s independence is that the Fed has long been a terrible manager of the nation’s money. The Fed was founded in 1913 and over the course of its existence has reduced the value of a dollar to less than 3 cents today. It’s so awful that pennies have become actually worthless.

With this track record, the Fed doesn’t have much credibility about which to brag.

Looking back at the record of price increases across a century, we observe a startling thing. The value of the dollar fell precipitously from 1913 to 1920. Indeed, it lost fully half its value in the years following the Fed’s founding.

It’s fascinating how little public consciousness of this exists today. This is because during those war years, there was so much else happening that simply overshadowed how money dramatically lost its value. We had progressivist politics running roughshod over the Constitution and American tradition. We had the war and conscription. We had price controls, censorship, and wartime planning.

In addition, in those days, we did not really have U.S. statistical agencies collecting data and broadcasting it out to the American public. There were newspapers but no radio or TV much less the internet, so this kind of information was hard to come by. One only knew what one knew.

A full deconstruction of this period appears in Benjamin Anderson’s marvelous 1948 book “Economics and the Public Welfare.” Here is your source for all that you need to know.

As he explains, business conditions generally seemed solid. Stock markets were rocking and profits were high. Dividends were rolling in and the wealthy were getting wildly rich off the war in particular. Exports boomed because Europe needed food, machines, steel, and munitions. The United States has never experienced such a high trade surplus.

The United States entered the war in 1917 and the war boom continued. Jobs were plentiful. The draft was disrupting normal community life. Censorship was pervasive and it became clear that the United States would be in a position to redraw the map of Europe after the war. Times seemed good all around, or, at least, they were so disruptive that people hardly noticed that half their purchasing power was being drained away.

The Fed assisted in providing liquidity to Europe and to companies making goods for the war, plus the U.S. government was selling bonds. In this, the United States deployed some of the most shocking war propaganda in history. Here is an ad for war bonds that I spotted at an antique store last week. I marveled at the symbolism and manipulation of every base sensibility.

All the expansion of government spending, credits to exporters, credits to foreign importers, demand boosts, and guarantees of war bonds put upward pressure on prices. These were huge factors. But none of these compares with the truly surprising source of the inflation, which was not traceable to the Fed as such. It was the import of gold.

This requires some explanation, one that reveals a key fact about how international money flows operated in the past.

Under the gold standard, all industrialized nations and most countries had national monies that were convertible into gold. In other words, the names on the currencies were brands but the composition of them all was the same. This greatly assisted in facilitating global trade flows. One nation would sell goods to another nation and get gold in exchange.

This was how the world worked even after the Fed was created. The gold standard in some form existed for centuries but became codified into U.S. monetary practice in 1873, thus settling a long struggle between silver and gold for domination.

With the United States on a gold standard, all exports were paid in gold. As a result, gold flows shifted inward and dramatically so. The United States was running a huge trade surplus; that is, the value of exports greatly exceeded the value of imports. The result was a massive increase in base money from 1914 through 1918.

What happens under such conditions? We know from both history and theory. When the Spanish Empire discovered and returned gold from the Americas, Spain experienced an epic inflation; that is, the value of each existing unit of money was reduced by the increase in its quantity.

The result is a large increase in prices. None of this is surprising. Indeed, that is precisely how the system is supposed to work. Nations that persistently exported much more than they imported would naturally experience upward price pressure. The reverse happens in the countries that import. They experience declining price pressure (provided there are not other factors at work).

How does this system facilitate trade? It means there is a tendency toward international market clearing. The exporting nations experience higher costs that eventually trigger factors that reverse trade flows. Their goods and costs of production become too high and demand falls; meanwhile, importing nations begin to experience lower costs and better economic conditions.

This is the reason that for centuries, trade between nations would tend to balance out, with no single country enjoying a permanent advantage over any other. It was on this basis that the 19th century economist David Ricardo posited the “law of one price.” His observation is that over the long run, goods, wages, services, and even commodities would tend to track toward the same level.

In technical economic terms, this was deemed the price-specie flow mechanism. It was the basis of free trade and the foundation of the claim that such a system would be great for everyone over the long term.

In other words, most of the inflation the United States experienced from 1914 through 1920 was simply the mechanism in operation. Gold imports and goods exports lead to higher prices. This would be true whether the Fed existed or not. It was a simple matter of trade flows.

This system actually worked very well. It meant that no country had a permanent advantage in competitive production over any other, because the price system adjusted. This was a main advantage of the gold standard.

That system came under attack throughout the rest of the century, between 1933 and 1944 in particular, culminating in the Nixon shock of 1971 and the inauguration of the fiat dollar system in 1973. After that, the demand for U.S. dollars abroad became essentially unlimited. There were no more shipments of gold and international price adjustments simply stopped taking place.

Prices in the United States rose higher and higher, ruining U.S. export markets and causing a permanent shift in U.S. trading relations. Today, the rest of the world enjoys a massive price and cost advantage over the United States, which Trump is trying to address through tariffs. It’s a Band-Aid approach that does not address the actual structural problem.

What we actually need is a restoration of gold as international money. Nor is bitcoin a viable substitute; indeed, a bitcoin standard would likely be an invitation to the surveillance state to create programmable money that is even more dependent on U.S. debt than the current system.

If we study precisely why the United States experienced such a huge inflation during and after the Great War all those years ago, we gain insight into how trade flows worked at a time when money was relatively more sound than it is today. The inflation in those days was not a sign of a broken system but an indication that the system was working as it should.

There are costs to government intervention. Inflation is one of them. This was the hidden cost of war. Business was booming. Stocks were soaring. Exports were never better. Meanwhile, the purchasing power of the dollar experienced steep declines, harming economic prospects for average people even as the rich got richer.

Little did we know in those days that what we experienced was just the beginning. It would be a foreshadowing of a full century of inflation and loss of liberty.

Will firing the Fed chairman fix the problem? No. But it could at least begin a period in which this institution is finally held accountable. This is surely a good thing.

Views expressed in this article are the opinions of the author and do not necessarily reflect the views of The Epoch Times.

Friends Read Free

Copy

Facebook

Tweet

Friends Read Free

Copy

Facebook

Tweet