Commentary

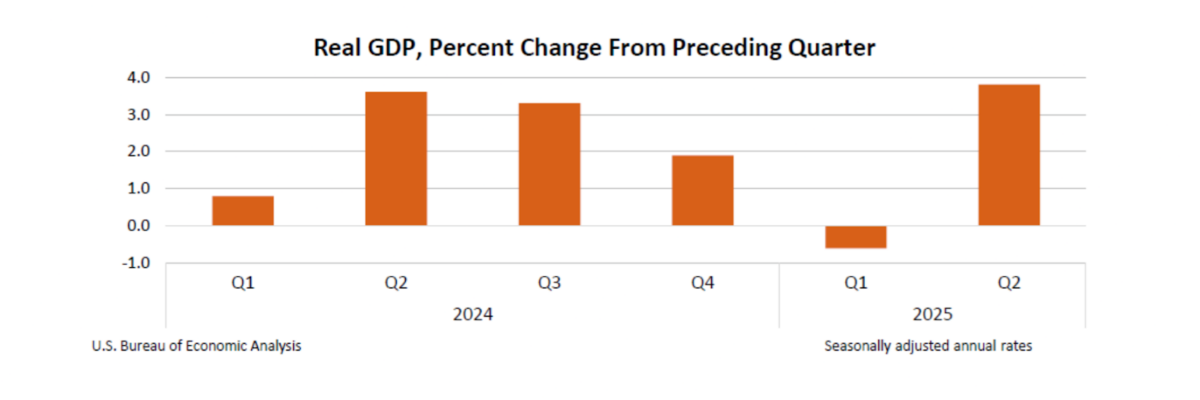

The second quarter gross domestic product (GDP) report came out last week. The growth registered in real terms at a very impressive 3.8 percent. This follows the previous quarter which was down. It seems that we are once again avoiding a technical recession. The Trump administration earned a talking point for a few days, and there is a sense of relaxation in markets that the tariff wars are not going to destroy the economy after all.

Even so, the enthusiasm for the new report was muted at best. This is for a reason. Once you dig into the data, the source of the strength is more technical and incidental than substantial. In other words, this new report follows the trend of five years, which is that the old markers don’t seem to be marking much anymore.

The notable change that boosted the GDP this time was a collapse in imports. This is a bit odd if you think about it. Imports are intermediate goods and retail goods that people buy. It is not entirely obvious why importing less should necessarily translate to higher economic output. And yet, that is how the GDP was set up in the 1930s: Imports subtract, and exports add.

What we really should be looking for is business investment. And here we find something interesting and a bit alarming. It is down and dramatically so. This is deeply worrisome.

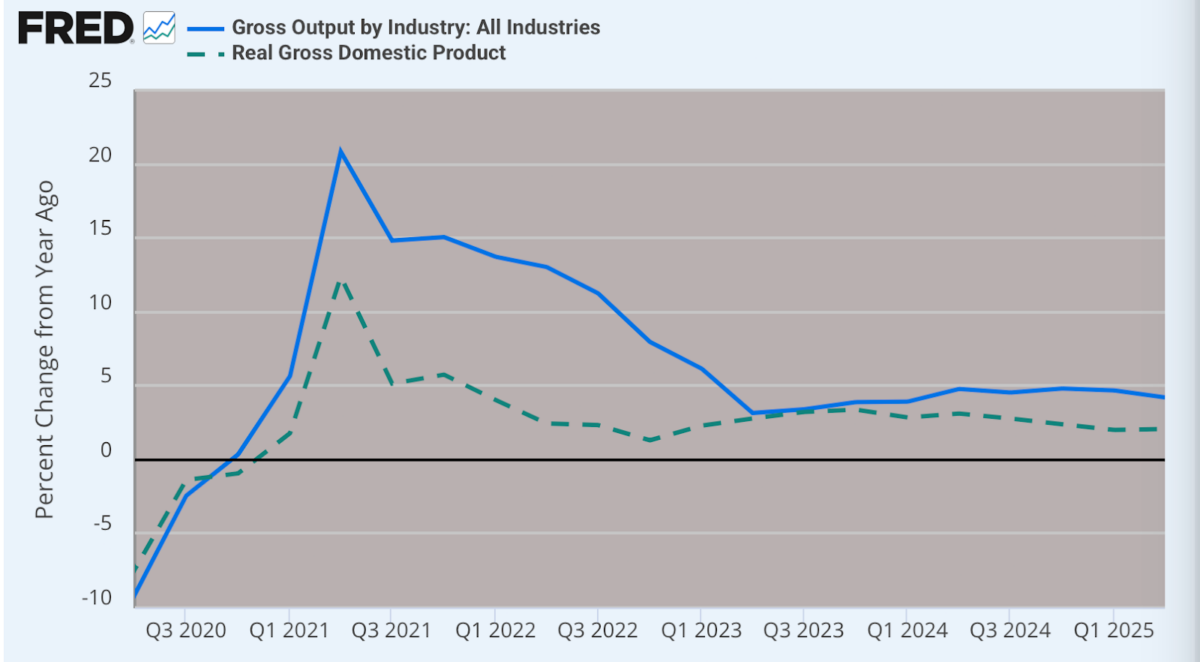

Mark Skousen noted: “[Gross output] revealed that economic growth is slowing to a crawl, ahead only 1.2 percent in real terms. If you include all transactions in wholesale and retail trade, the adjusted GO is up only 0.3 percent. More important, overall business spending fell sharply, by an annualized 5.6 percent in real terms. These results are much more consistent with the weak labor-market data.”

Indeed, gross output is trending down.

Just how extreme was the impact of the imported goods collapse? It completely reversed what would have otherwise been a quarter of dramatically declining output.

David Stockman explains: “During Q2 everything else—personal consumption, business investment, housing, government and inventories—netted to a -1.23 percent annual rate during the quarter. So thanks to the aberrantly large import drop during Q2 what would have otherwise been a loser quarter got transformed into a ‘Great Numbers’ headline.”

Even more worrisome is that the meager levels of business investment mostly trace to activity within the artificial-intelligence sector. It is looking ever more like a perpetual motion machine, with new investments rooted in leverage obtained with nonexistent collateral marked by paper-money illusions. This in turn is driving financial markets.

For all the world, this looks like the gathering of another financial boom-bust to parallel the 2000-era dotcom mess and the housing crisis of 2008 except on a bigger and more existentially meaningful scale. All of this is obvious from the data, which is precisely why keen observers of the details were not exactly celebrating newfound prosperity.

Hence, despite the headline numbers, there is plenty of reason for concern.

We have to remember that the Trump administration did not start with a healthy economic environment. It inherited a recession that was covered up by data manipulation of labor market numbers plus the economic chaos of the COVID-19 pandemic years. Since 2020, the rise in government spending and monetary printing has been without any precedent in size and scale in U.S. history. All of this had a wildly distorting effect on business investment and the way it is and is not reported.

The previous administration had constructed a hall of mirrors. This is what Trump inherited. Instead of merely cutting taxes and regulations, he embarked on a new experiment of raising tariffs to a level not seen since 1930, with the expectation that this would boost investment in the United States. So far it has not. One might have wished he had postponed this experiment in protectionism until we were back on a more solid growth path.

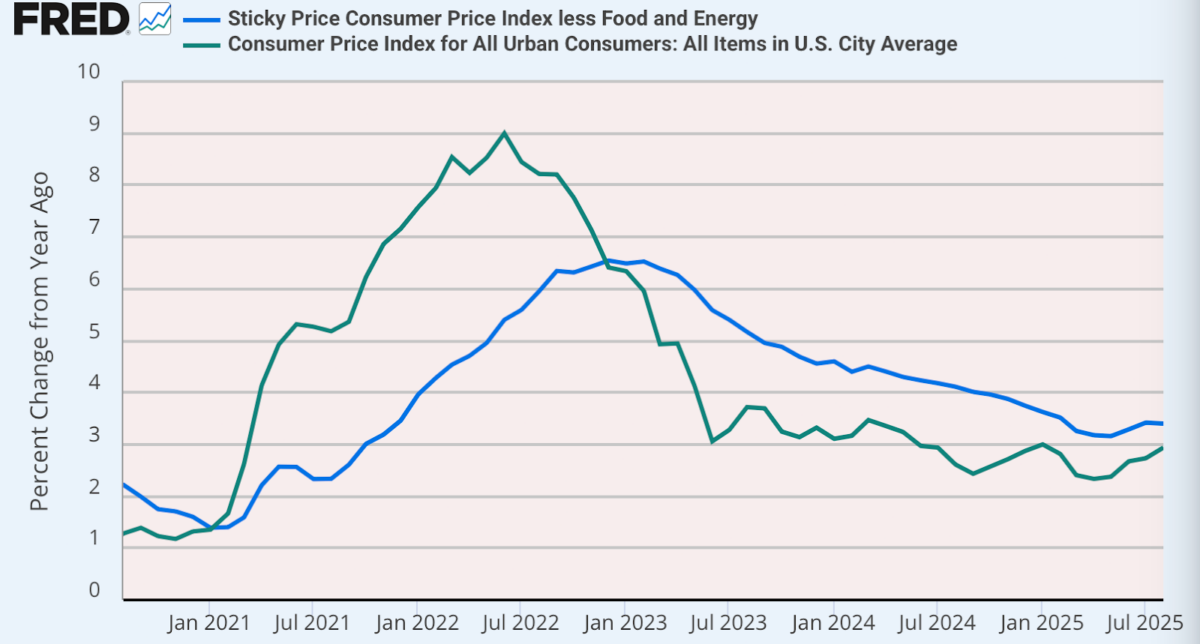

In this period, the U.S. dollar lost 25 percent to 35 percent of its purchasing power, devastating real income in ways that have been largely disguised by bad data. Americans went for years thinking that the high prices would return to normal once the crisis ended. That was never going to happen but the new reality set in slowly. Essentially, we’ve undergone a huge devaluation.

The worst part is that the rise in prices has not been tamed. We are still running 50 percent to 75 percent ahead of target inflation rates. That’s why it seems like matters are getting worse gradually rather than quickly. Not losing as much money is not the same as entering back on a growth path.

The trend line of lower inflation that we saw just after inauguration is no longer with us. That turned out to be a brief illusion. The great worry now is that we might be headed into a second wave of inflation. That would wreck American living standards, and might take the entire Trump administration down with it.

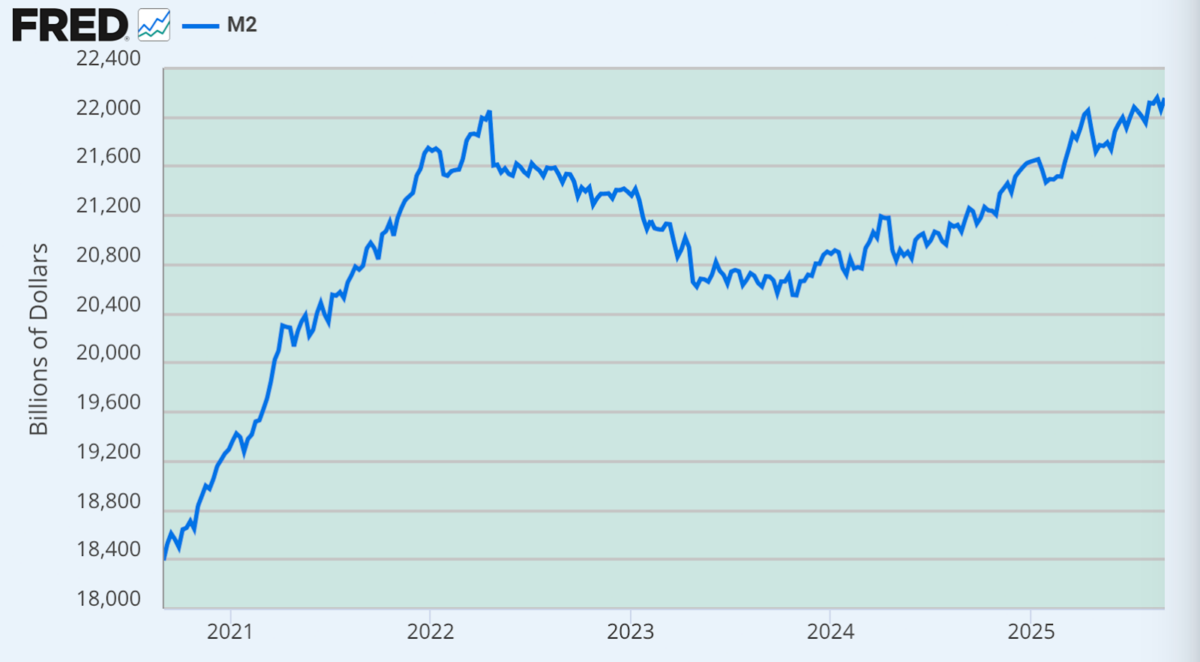

So far, the Federal Reserve has resisted pressure to make dramatic changes in its interest rate policy. That’s good. But it did make one concession to political pressure. It lowered rates by a quarter point, which amounts to a cosmetic change.

That said, the money supply as measured by M2 has just crossed into symbolically dangerous territory. It is now exceeding its 2021 high and growing 4.6 percent per year. In the models, that should end up generating inflation insofar as its rate of growth outstrips output. But given that we don’t really even have accurate output numbers, it’s truly anyone’s guess how this ends up.

So far, real-time inflation rates don’t seem dangerously high, but that is no reason to relax and forget about the issue. In the 1970s, sure as the Fed and the public believed one round was over, another round began, until the devastation of 1979 led to a dramatic political revolution.

This combination of illusory output growth, simmering inflationary pressure, and labor shortage due to immigration crackdowns poses some serious risks to Trump-era prosperity. This might even be the biggest risk the administration faces today. I shudder to imagine what would replace Trump should things go really south in financials, output, and inflation.

The stakes are extremely high. A second-wave inflationary recession could lead to a dramatic political upheaval with dangerous results.

Views expressed in this article are the opinions of the author and do not necessarily reflect the views of The Epoch Times.

Friends Read Free

Copy

Facebook

Tweet

Friends Read Free

Copy

Facebook

Tweet